Medicare and respiratory care coverage is defined as the set of benefits under Medicare Parts A and B that pay for home oxygen therapy, respiratory assist devices, pulmonary rehabilitation, and related services for beneficiaries with documented chronic respiratory conditions. For seniors managing conditions like COPD or chronic respiratory failure, these benefits can mean the difference between affordable care and staggering out-of-pocket costs. The 2026 Medicare framework includes specific eligibility thresholds, cost-sharing rules, and billing standards set by the Centers for Medicare and Medicaid Services (CMS) that every beneficiary should understand before accepting equipment or scheduling therapy.

What respiratory care services does Medicare cover?

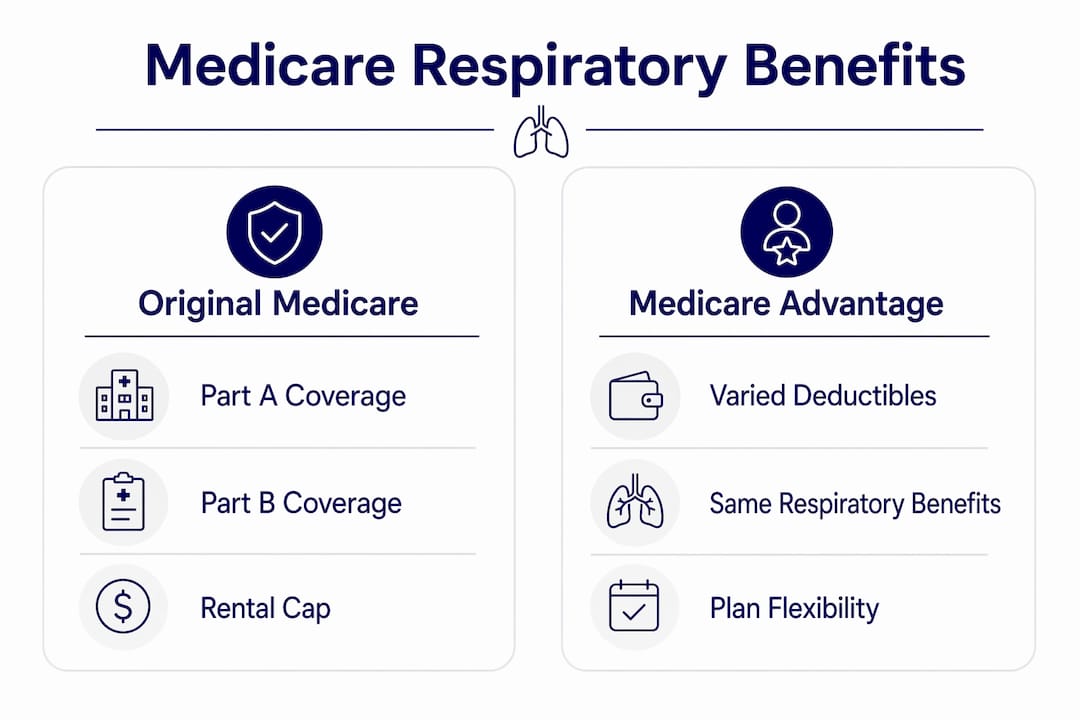

Medicare Part B covers home oxygen therapy, respiratory assist devices, and outpatient pulmonary rehabilitation programs. Medicare Part A covers respiratory care delivered during inpatient hospital stays and skilled nursing facility (SNF) stays as part of a bundled payment. These two parts work together, but they operate under very different rules.

The distinction between stationary and portable oxygen equipment matters more than most beneficiaries realize. Portable oxygen coverage requires qualifying test results based on resting oxygen levels, not just sleep studies. If your physician documents only nocturnal hypoxemia, Medicare covers stationary oxygen equipment but will not pay for a portable unit. That is a meaningful limitation for anyone who wants to stay active outside the home.

Conditions that commonly qualify beneficiaries for Medicare respiratory support include:

- COPD (Chronic Obstructive Pulmonary Disease): The most frequent qualifying diagnosis for home oxygen and respiratory assist devices.

- Chronic respiratory failure: Documented low blood oxygen levels at rest qualify under Group I criteria.

- Pulmonary hypertension and interstitial lung disease: May qualify under Group II or Group III tiers depending on test results.

- Obstructive sleep apnea: Can qualify for respiratory assist devices like CPAP or BiPAP under specific LCD policies.

- Neuromuscular diseases: Conditions affecting breathing muscles may qualify for devices coded E0470 or E0471 under CMS compliance guidelines.

Pulmonary rehabilitation is covered under Part B for beneficiaries with moderate to very severe COPD. The program must be physician-supervised and provided in a Medicare-approved facility. Coverage for lung treatments in this category is one of the most underused benefits in the program.

How do beneficiaries qualify for Medicare respiratory equipment?

Qualification for home oxygen and respiratory assist devices follows a tiered system defined by CMS. Each tier requires specific blood oxygen measurements taken while the beneficiary is awake, at rest, and breathing room air. Testing during an acute flare-up does not count. The chronic stable state requirement exists because oxygen levels during illness are temporarily lower and do not reflect a beneficiary’s baseline need.

The three qualification tiers work as follows:

- Group I: Arterial PO₂ at or below 55 mm Hg, or oxygen saturation at or below 88% in a stable resting state. This is the most common coverage tier.

- Group II: Arterial PO₂ between 56 and 59 mm Hg, or oxygen saturation at 89%, combined with a qualifying condition such as dependent edema, erythrocythemia, or pulmonary hypertension.

- Group III: Arterial PO₂ at or below 55 mm Hg or oxygen saturation at or below 88% during exercise or sleep, when the beneficiary does not qualify at rest.

Beyond the blood oxygen thresholds, written orders and documented medical necessity are mandatory for Medicare reimbursement. Claims must include clinical indicators, ICD-10-CM diagnosis codes, and a physician signature. Missing any one of these elements is enough to trigger a denial.

Spirometry and pulmonary function tests must follow American Thoracic Society guidelines and require physician-signed reports. These tests are diagnostic, not therapeutic, and Medicare treats them accordingly. They establish the clinical foundation for all downstream equipment and therapy coverage.

Medicare Advantage respiratory benefits">

Medicare Advantage respiratory benefits">

Medicare caps rental coverage of home oxygen equipment at 36 months. After that cap, the supplier must continue providing the equipment and maintenance, but Medicare stops making rental payments. Recertification, including an in-person physician visit, is required at specific intervals to keep coverage active.

Pro Tip: Schedule your qualifying oxygen test during a period of clinical stability, not during a respiratory infection or hospitalization. A test taken during an acute episode may show artificially low oxygen levels that do not reflect your true baseline, which can complicate recertification later.

What costs should you expect for respiratory care in 2026?

The 2026 Medicare Part B deductible is $283. After meeting that deductible, you owe 20% coinsurance on the Medicare-approved amount for durable medical equipment (DME) such as home oxygen concentrators, respiratory assist devices, and related supplies. That 20% applies to rentals and purchases alike.

| Cost element | Original Medicare | Medicare Advantage |

|---|---|---|

| Part B deductible | $283 in 2026 | Varies by plan |

| DME coinsurance | 20% of approved amount | Often 20%, may differ |

| Prior authorization | Not typically required | Frequently required |

| Portable oxygen coverage | Based on qualifying tests | Plan-specific rules apply |

| Rental cap | 36 months | May vary |

The supplier you choose has a direct impact on your total cost. Suppliers who accept assignment must accept the Medicare-approved amount as full payment. They cannot bill you more than your standard coinsurance. A supplier who does not accept assignment can charge up to 15% above the Medicare-approved amount, which adds up quickly over a 36-month rental period.

Medicare Advantage plans cover the same core respiratory benefits as Original Medicare, but the rules differ. Many Advantage plans require prior authorization for DME, meaning your physician must get approval before you receive equipment. Costs and coverage limits vary by plan and by county. Beneficiaries in Southwest Florida should verify their specific plan’s rules before accepting any respiratory equipment or scheduling pulmonary rehabilitation.

Pro Tip: Before accepting any DME, ask the supplier directly: “Do you accept Medicare assignment?” If they hesitate or say no, contact your Medicare plan options advisor to find a participating supplier in your area.

How is respiratory therapy billed across different care settings?

The care setting where you receive respiratory therapy determines how Medicare pays for it. This distinction catches many beneficiaries and even some providers off guard.

Respiratory care services in SNFs are bundled under Medicare Part A. Therapists and outside agencies cannot submit separate bills for these services during a covered SNF stay. Any attempt to bill separately results in a denial. The bundled payment covers all care delivered during that stay, including respiratory therapy, physical therapy, and nursing services.

Home health respiratory therapy operates under a different and often misunderstood set of rules:

- CPT 99503 standalone billing under traditional Medicare for home health respiratory therapy is generally denied. These services are bundled within episode-based home health payments.

- Incorrect billing of CPT 99503 can trigger audits and compliance reviews for the provider. Beneficiaries are not directly penalized, but denied claims delay care.

- A written physician plan of care is required for all home health therapy reimbursement. Without it, no claim will be paid regardless of the services delivered.

- Medicare Advantage plans may reimburse respiratory therapy services differently than Original Medicare, often requiring prior authorization and limiting standalone billing for certain therapy codes.

- Outpatient pulmonary rehabilitation under Part B is billed separately and does not fall under the home health bundling rules. This is the clearest path to standalone respiratory therapy coverage.

Understanding which setting applies to your care prevents surprise denials. If your physician recommends respiratory therapy, ask specifically whether it will be delivered in an outpatient facility, at home under a home health agency, or during a facility stay. Each setting triggers a different billing pathway and a different set of coverage rules.

Key Takeaways

Medicare covers respiratory care through Parts A and B, but eligibility, costs, and billing rules vary significantly by care setting, equipment type, and plan.

| Point | Details |

|---|---|

| Qualification thresholds matter | Group I coverage requires arterial PO₂ at or below 55 mm Hg or oxygen saturation at or below 88% in a stable state. |

| Portable oxygen is not automatic | Nocturnal hypoxemia alone qualifies you for stationary oxygen only, not portable units. |

| 2026 cost-sharing is predictable | The Part B deductible is $283, followed by 20% coinsurance on Medicare-approved DME amounts. |

| Rental caps end payments, not service | After 36 months, Medicare stops rental payments but the supplier must continue providing equipment. |

| Care setting drives billing rules | SNF respiratory care is bundled under Part A; outpatient pulmonary rehab is billed separately under Part B. |

What I’ve learned about respiratory coverage denials

After working with seniors across Southwest Florida on Medicare coverage decisions, one pattern stands out clearly. The beneficiaries who run into the most trouble are not the ones with the most complex conditions. They are the ones who assumed their physician and their supplier had everything handled.

Respiratory coverage denials almost always trace back to documentation gaps, not medical ineligibility. A qualifying test performed during a hospitalization instead of a stable outpatient visit. A supplier who did not accept assignment. A recertification visit that was missed because no one flagged the deadline. These are preventable problems, and they cost beneficiaries real money.

The Medicare Advantage variable is the one I find most underappreciated. Beneficiaries who switch from Original Medicare to an Advantage plan often do not realize their respiratory equipment authorization rules have changed until they receive a denial letter. Verifying plan-specific coverage rules before enrollment, not after, is the move that protects you.

My honest advice: treat your recertification calendar like a bill due date. Put it in writing, share it with a family member, and follow up with your physician’s office at least 60 days before the deadline. Medicare’s rental cap and recertification requirements are not flexible. Missing a deadline means losing coverage, and reinstating it requires starting the qualification process over.

— Alston

Xactinsure helps Southwest Florida seniors with respiratory coverage

Sorting through Medicare’s respiratory care rules is genuinely complex, and the stakes are high when you depend on oxygen equipment or pulmonary therapy every day. Xactinsure works with seniors across Fort Myers, Cape Coral, Naples, and neighboring counties to match them with Medicare plans and supplements that fit their specific health needs, including coverage for respiratory care equipment and services.

Xactinsure offers free educational seminars and no-obligation consultations to help you understand your options before you commit to a plan. Whether you are weighing Original Medicare against a Medicare Advantage plan, or looking at a Medigap Plan G to cover your 20% coinsurance on DME, the team at Xactinsure can walk you through the numbers. Reach out to schedule a consultation and get answers specific to your situation.

FAQ

What does Medicare Part B cover for respiratory care?

Medicare Part B covers home oxygen therapy, respiratory assist devices, and outpatient pulmonary rehabilitation for beneficiaries with documented qualifying conditions. Coverage requires meeting CMS medical necessity criteria and using a supplier who accepts Medicare assignment.

How do I qualify for home oxygen under Medicare?

Group I qualification requires arterial PO₂ at or below 55 mm Hg or oxygen saturation at or below 88% measured while awake, at rest, and in a clinically stable state. Testing during an acute illness or hospitalization does not satisfy this requirement.

Does Medicare cover portable oxygen equipment?

Medicare covers portable oxygen only if your qualifying test results are based on resting oxygen levels. If your physician documents only nocturnal hypoxemia, Medicare covers stationary oxygen but not a portable unit.

How long does Medicare pay for rented oxygen equipment?

Medicare pays for home oxygen equipment rentals for up to 36 months. After that cap, the supplier must continue providing the equipment and maintenance, but Medicare stops making rental payments. Recertification is required at set intervals to maintain coverage throughout the rental period.

Do Medicare Advantage plans cover respiratory therapy the same way?

Medicare Advantage plans cover the same core respiratory benefits as Original Medicare but often require prior authorization and may apply different billing rules for respiratory therapy services. Beneficiaries should verify their specific plan’s policies before accepting equipment or scheduling therapy.

Recommended

- Medicare Options for Aging Parents: 2026 Family Guide | XactInsure Blog

- Insurance Articles & Guides - XactInsure Blog

- Medicare Costs Every Family Should Understand in 2026 | XactInsure Blog

- How to Prepare for a Medicare Coverage Review Meeting | XactInsure Blog

Get a Free Professional Insurance Review

Our licensed Southwest Florida specialists serve Lee, Collier, and Charlotte counties with local, family-first protection advice.

Request Free Consultation →