Medicare managed care is defined as a system where private insurers, approved by the Centers for Medicare and Medicaid Services (CMS), deliver Medicare benefits through coordinated care networks known as Medicare Advantage (Part C) plans. These plans replace Original Medicare Parts A and B with a single, integrated coverage structure. Most also include Part D prescription drug coverage and extra benefits like dental, vision, and hearing. If you are turning 65 or newly eligible for Medicare, understanding what is medicare managed care is the first step toward making a confident coverage decision.

How do Medicare managed care plans work?

Medicare managed care plans replace Original Medicare with a private plan that delivers the same core benefits, often with added features. CMS pays the private insurer a fixed monthly amount per enrollee. The insurer then manages your care through a network of doctors, hospitals, and specialists.

To enroll, you must meet four requirements:

- Active Medicare Part A and Part B enrollment

- Residency within the plan’s service area

- U.S. citizenship or lawful presence

- Enrollment during an approved election period

The election periods that govern enrollment include the Initial Coverage Election Period (when you first become eligible), the Annual Coordinated Election Period (october 15 through december 7 each year), the Medicare Advantage Open Enrollment Period (january 1 through march 31), and Special Election Periods triggered by qualifying life events such as moving or losing employer coverage.

Missing your window matters. Missed election periods can delay your coverage start date and leave you without protection during the gap. Acting within the correct period is not optional. It is the single most common mistake new beneficiaries make.

Pro Tip: Set a calendar reminder 90 days before your 65th birthday. Your Initial Coverage Election Period begins three months before your birth month and ends three months after it.

What are the main differences between Medicare managed care and Original Medicare?

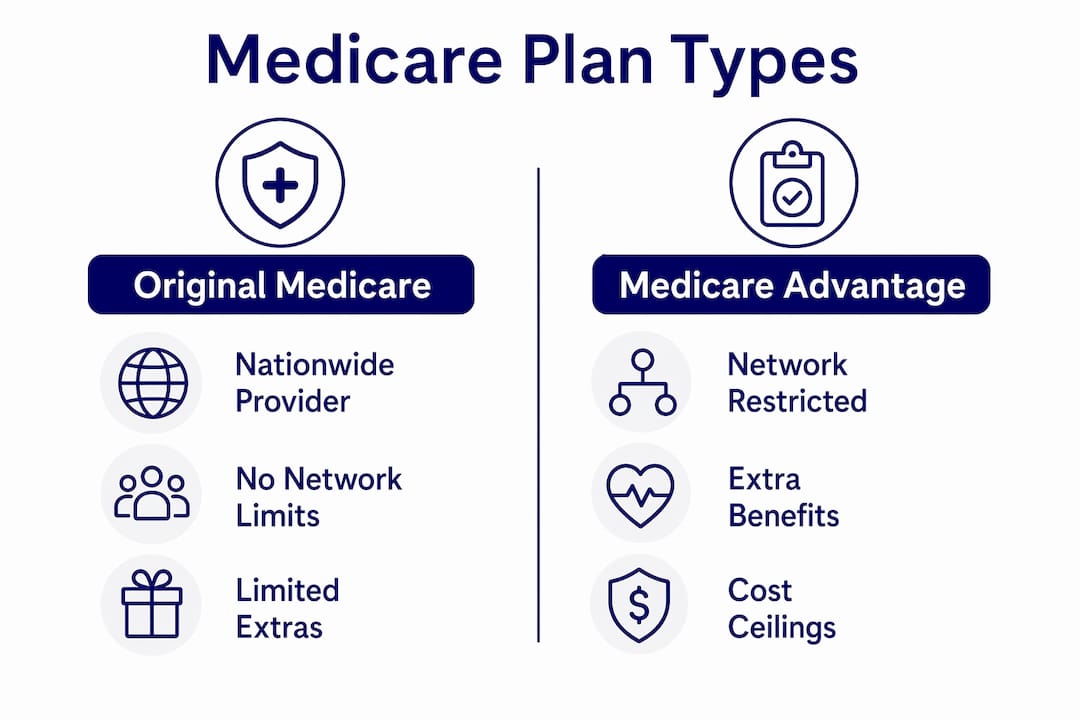

The core difference between Medicare Advantage and Original Medicare is provider access. Original Medicare lets you see any doctor or hospital in the country that accepts Medicare. Managed care plans restrict you to a network. That restriction is the price of the added benefits and cost controls these plans offer.

Medicare Advantage networks limit enrollees to roughly half the physicians available under traditional Medicare in a given area on average. That is a significant reduction. If your cardiologist or orthopedic surgeon does not participate in the plan’s network, you may need to switch providers or pay out-of-network rates.

| Feature | Original Medicare | Medicare Advantage |

|---|---|---|

| Provider access | Any Medicare-accepting provider | Network-based (HMO or PPO) |

| Referrals required | No | Often yes, especially HMOs |

| Drug coverage | Separate Part D plan needed | Usually bundled |

| Dental, vision, hearing | Not covered | Often included |

| Out-of-pocket cap | None | Required by law |

| Billing | Multiple bills from providers | Single plan manages billing |

Medicare Advantage plans frequently include benefits that Original Medicare does not cover at all. Vision exams, hearing aids, dental cleanings, and fitness memberships are common additions. Most plans also bundle Part D drug coverage, eliminating the need for a separate prescription plan.

The trade-off is real. You gain extra benefits and a predictable cost ceiling. You give up the freedom to see any Medicare provider without restriction. For beneficiaries who see a small number of trusted doctors and want lower monthly costs, managed care often makes financial sense. For those who travel frequently or need access to specialists across multiple states, Original Medicare may serve them better.

How do costs and out-of-pocket limits work in Medicare managed care plans?

Medicare Advantage plans combine Part A and Part B costs under one plan with a legally required annual out-of-pocket maximum. Original Medicare has no such cap, which means a serious illness can generate unlimited cost exposure.

For 2026, out-of-pocket limits may not exceed $9,250 for in-network services and $13,900 for combined in-network and out-of-network services. These are federal ceilings. Individual plans may set lower limits, and many do. Once you hit your plan’s cap, the plan covers 100% of covered services for the rest of the year.

| Cost Type | In-Network Cap (2026) | Combined In/Out Cap (2026) |

|---|---|---|

| Maximum allowed by law | $9,250 | $13,900 |

| Applies to | Parts A and B services | Parts A, B, and out-of-network |

| Prescription drugs | Separate cost-sharing rules | Separate cost-sharing rules |

Prescription drug costs operate under separate rules. The out-of-pocket cap applies only to Part A and B services. Drug costs are governed by the plan’s Part D formulary, which assigns medications to tiers with different copay levels. A plan with a $0 premium and a low medical cap may still carry significant drug cost-sharing for brand-name medications.

Budget for medical and drug costs separately when comparing plans. Look at your current prescriptions, find each drug on the plan’s formulary, and calculate your estimated annual drug spend before you enroll.

Pro Tip: Ask the plan directly for its Summary of Benefits document. It lists every copay, coinsurance rate, and drug tier in plain language. Compare at least two plans side by side before deciding.

What should beneficiaries consider when choosing a Medicare managed care plan?

Choosing the right managed care plan starts with your doctors, not your premium. A $0 premium plan means nothing if your primary care physician and specialists are not in the network.

Follow these steps before enrolling:

- List your current providers. Write down every doctor, hospital, and specialist you see regularly.

- Check each provider’s network status. Call the plan directly or use the plan’s online directory to confirm participation.

- Review your medications. Pull up the plan’s formulary and confirm your drugs are covered at an acceptable tier.

- Estimate your total annual cost. Add premiums, expected copays, and estimated drug costs. Compare that number across plans.

- Use Medicare Plan Finder. The official Medicare.gov tool lets you compare Medicare Advantage, Part D, and Medigap options by cost, coverage, and provider availability. You can also enroll in Medicare Advantage plans directly through the site.

Beyond the checklist, consider how often you use healthcare. Beneficiaries with frequent specialist visits or chronic conditions may hit their out-of-pocket cap regularly, making a lower cap more valuable than a lower premium. Beneficiaries in good health who rarely see doctors may benefit most from a $0 or low-premium plan with basic coverage.

Provider network size and composition vary widely across plans, even within the same county. Two plans from the same insurer in Fort Myers or Naples may include completely different hospital systems. Never assume a plan covers your preferred providers. Verify every name before you sign.

Beneficiaries who want broader provider access without network restrictions may also want to review Medicare Supplement Plan N as an alternative to managed care. It pairs with Original Medicare and covers many out-of-pocket costs without limiting your provider choice.

Key takeaways

Medicare managed care, formally known as Medicare Advantage, delivers Medicare benefits through private insurer networks with an annual out-of-pocket cap, added benefits, and restricted provider access compared to Original Medicare.

| Point | Details |

|---|---|

| Core definition | Medicare managed care means Medicare Advantage plans from CMS-approved private insurers. |

| Enrollment requirements | You need Parts A and B, plan-area residency, and enrollment within a valid election period. |

| Out-of-pocket cap | 2026 in-network cap is $9,250; drug costs are tracked separately under Part D rules. |

| Provider access trade-off | Managed care networks cover roughly half the physicians available under Original Medicare. |

| Plan selection priority | Verify your doctors and medications before comparing premiums or plan names. |

My honest take on choosing Medicare managed care

After working with Medicare beneficiaries across Southwest Florida for years, I have seen one mistake repeat itself more than any other. People choose a plan based on the premium and discover later that their doctor is not in the network. That discovery usually comes at the worst possible moment, right before a procedure or during a specialist referral.

The marketing around Medicare Advantage is loud and often misleading. A $0 premium plan is not free. It shifts costs to copays, coinsurance, and drug tiers. The math only works in your favor if you understand the full picture before you enroll.

The other thing I tell every beneficiary: do not skip the annual review. Plans change their networks, formularies, and cost structures every year. A plan that worked perfectly in 2025 may have dropped your cardiologist or moved your blood pressure medication to a higher tier by january 2026. The Annual Coordinated Election Period exists for a reason. Use it.

Official tools like Medicare Plan Finder are genuinely useful, but they work best when you already know your providers and medications. Pair the tool with a conversation with a licensed agent who works with multiple carriers. That combination gives you both the data and the interpretation.

— Alston

How Xactinsure helps with Medicare managed care decisions

Choosing between Medicare Advantage plans, Medigap options, and standalone Part D coverage is not a decision you should make alone. Xactinsure specializes in Medicare coverage guidance for seniors across Southwest Florida, including Fort Myers, Cape Coral, Naples, and surrounding counties.

Xactinsure works with multiple carriers to compare plans side by side without favoring any single insurer. Whether you are enrolling for the first time or reviewing your current plan before the next election period, the team offers free, no-obligation consultations tailored to your health needs and budget. Seniors in the region can also attend free educational seminars to ask questions and get clear answers before making any decisions. Reach out to schedule a consultation and get the clarity you deserve.

FAQ

What is Medicare managed care in simple terms?

Medicare managed care refers to Medicare Advantage (Part C) plans offered by private insurers approved by CMS. These plans replace Original Medicare with coordinated coverage through a provider network, often including drug, dental, and vision benefits.

How does Medicare Advantage differ from Original Medicare?

Original Medicare lets you see any provider that accepts Medicare nationwide. Medicare Advantage restricts you to a plan network, typically an HMO or PPO, but adds an annual out-of-pocket cap and often includes extra benefits Original Medicare does not cover.

What are the 2026 out-of-pocket limits for Medicare Advantage?

Federal law caps in-network out-of-pocket costs at $9,250 and combined in/out-of-network costs at $13,900 for 2026. Individual plans may set lower limits. Prescription drug costs are not included in these caps and are governed separately.

Can I switch Medicare Advantage plans after I enroll?

You can switch during the Annual Coordinated Election Period (october 15 through december 7) or the Medicare Advantage Open Enrollment Period (january 1 through march 31). Special Election Periods apply for qualifying life events like moving or losing other coverage.

Is Medicare Plan Finder the best way to compare plans?

Medicare Plan Finder on Medicare.gov is the official tool for comparing Medicare Advantage and Part D plans by cost, coverage, and provider availability. Pairing it with guidance from a licensed agent who represents multiple carriers gives you the most complete comparison.

Recommended

- Medicare Insurance Plans in Golden Gate

- Medicare Insurance Plans in Cape Coral, Florida

- Medicare Insurance Plans in San Carlos Park

- Medicare Insurance Plans in Englewood, Florida

Get a Free Professional Insurance Review

Our licensed Southwest Florida specialists serve Lee, Collier, and Charlotte counties with local, family-first protection advice.

Request Free Consultation →