Medigap coverage is private supplemental insurance that pays for healthcare costs Original Medicare does not cover, including deductibles, coinsurance, and copayments. Sold by private insurers and regulated under federal standards, Medigap policies attach directly to Original Medicare Parts A and B. In 2026, the Part A inpatient deductible stands at $1,736 per benefit period, and Medicare Part B leaves you responsible for 20% of outpatient costs after your annual deductible. Without a supplement, those numbers add up fast. Medigap is not the same as Medicare Advantage. It works alongside Original Medicare, not as a replacement.

What is Medigap coverage and how does it work?

Medigap, formally called Medicare Supplement Insurance, pays after Original Medicare processes a claim. Medicare pays its approved share first. Your Medigap policy then covers some or all of the remaining cost, depending on which plan you hold.

The federal government standardizes Medigap plans into lettered options: Plan A, Plan B, Plan C, Plan D, Plan F, Plan G, Plan K, Plan L, Plan M, and Plan N. Every insurer selling Plan G must offer the exact same benefits as every other insurer selling Plan G. What differs is the monthly premium. That standardization is the most underappreciated feature of Medigap insurance. You are comparing price, not hidden benefit differences.

All Medigap plans cover Medicare Part A coinsurance and hospital costs for up to 365 days beyond Medicare’s benefit period limit. That extended inpatient protection matters most if you face a serious illness or prolonged hospital stay.

What Medigap typically covers

- Medicare Part A coinsurance and extended hospital costs (365 days beyond Medicare limits)

- Medicare Part B outpatient coinsurance, generally 20% of approved costs

- Part A hospice care coinsurance or copayments

- Blood transfusions (first three pints)

- Skilled nursing facility coinsurance (on select plans)

- Part A and Part B deductibles (on select plans)

- Foreign travel emergency care (on select plans, with limits)

What Medigap does not cover

Medigap policies exclude prescription drugs, long-term care, vision, dental, and hearing aids. These are significant gaps. You will need a separate Medicare Part D plan for prescription drug coverage. Dental and vision require standalone policies or a Medicare Advantage plan, which is a different product entirely.

Pro Tip: If you are comparing Medigap to Medicare Advantage, remember they are not interchangeable. Medigap supplements Original Medicare. Medicare Advantage replaces it. You cannot hold both simultaneously.

Foreign travel emergency benefits

Medigap foreign travel coverage pays 80% of emergency costs abroad after a $250 annual deductible, up to a $50,000 lifetime maximum. Original Medicare provides almost no coverage outside the United States. For seniors who travel internationally, this benefit alone can justify the monthly premium.

What types of Medigap plans exist and how do you compare them?

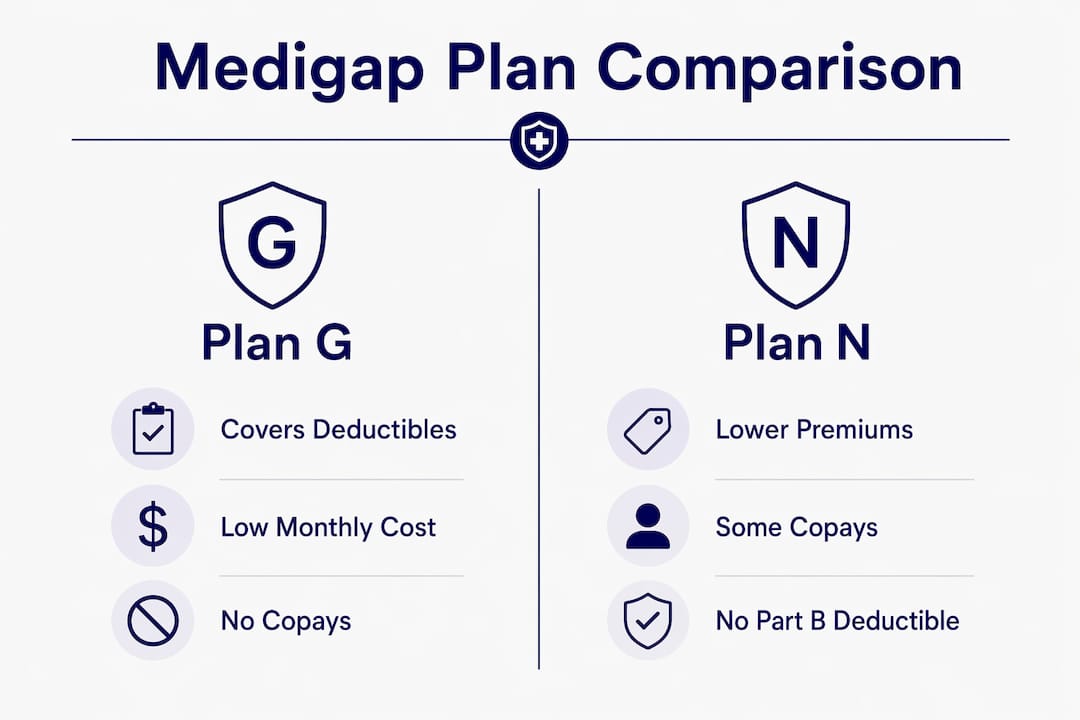

Plan G and Plan N are the most widely purchased Medigap plans available to new enrollees today. Plan F was the most comprehensive option historically, but it is no longer available to beneficiaries who became eligible for Medicare after january 1, 2020.

Plan G covers nearly all Medicare cost-sharing except the Part B annual deductible, which is $283 in 2026. Seniors who see specialists frequently or want maximum predictability in their healthcare costs benefit most from Plan G. The tradeoff is a higher monthly premium.

Plan N is budget-friendly but carries some copays. Office visits may require a copay of up to $20, and emergency room visits not resulting in inpatient admission may require a $50 copay. Plan N also does not cover Medicare Part B excess charges, which are the amounts a provider can bill above Medicare’s approved rate.

Side-by-side plan comparison

| Feature | Plan G | Plan N |

|---|---|---|

| Part A coinsurance and hospital costs | Covered | Covered |

| Part B coinsurance | Covered | Covered (with copays) |

| Part A deductible | Covered | Covered |

| Part B deductible | Not covered | Not covered |

| Part B excess charges | Covered | Not covered |

| Foreign travel emergency | Covered (80%, $50,000 max) | Covered (80%, $50,000 max) |

| Skilled nursing facility coinsurance | Covered | Covered |

Plan G premiums typically range from $150 to $250 per month depending on your age and location. That range reflects how much premiums vary across insurers for the identical benefit set. Shopping multiple carriers for the same plan letter is the single most effective way to reduce your monthly cost without sacrificing coverage.

When and how should you enroll in Medigap?

Timing your Medigap enrollment correctly protects both your coverage and your wallet. The rules are specific, and missing the right window has real consequences.

-

Enroll during your Open Enrollment Period. This six-month window begins the month you turn 65 and are enrolled in Medicare Part B. During this period, insurers must accept you regardless of your health history. No medical underwriting applies.

-

Understand guaranteed issue rights. Certain life events, such as losing employer coverage or your Medicare Advantage plan leaving your area, trigger guaranteed issue rights outside the standard enrollment window. These rights give you temporary protection similar to Open Enrollment.

-

Recognize the risk of waiting. Outside the Open Enrollment Period, insurers can deny your application or charge higher premiums based on your health conditions. A pre-existing condition that seems minor today could result in a declined application tomorrow.

-

Act before health changes occur. Many seniors delay enrollment because they feel healthy and want to avoid the monthly premium. That logic reverses the moment a diagnosis arrives. At that point, getting coverage at a standard rate becomes difficult or impossible.

Pro Tip: The best time to buy Medigap is during your Open Enrollment Period. You will never again have the same guaranteed access to every plan at standard rates.

Practical tips for choosing and using your Medigap plan

Selecting the right Medigap policy requires matching the plan’s benefits to your actual healthcare habits and financial situation. A few practical points make that process clearer.

- No network restrictions apply. Medigap has no provider networks, meaning you can see any doctor or specialist who accepts Medicare. That freedom is a meaningful advantage over Medicare Advantage plans, which typically restrict you to a local network.

- Verify provider acceptance. While Medigap itself has no network, confirm that your specific provider accepts your insurer’s Medigap policy. This is a rare issue but worth a quick call before your first appointment.

- Add Part D separately. Medigap does not cover prescription drugs. Budget for a standalone Medicare Part D plan alongside your Medigap premium.

- Weigh premium versus out-of-pocket exposure. A lower-premium plan like Plan N saves money monthly but exposes you to copays and excess charges. A higher-premium plan like Plan G eliminates most surprises. Run the numbers based on how often you use healthcare services.

- Review your plan annually. Your health needs and premium rates both change over time. Reviewing your Medigap coverage each year keeps your plan aligned with your actual situation.

Pro Tip: Request quotes from at least three carriers for the same plan letter before enrolling. The benefits are identical by law. The savings from choosing a lower-premium carrier are real and recurring every month.

Key takeaways

Medigap coverage is the most reliable way for Medicare beneficiaries to control out-of-pocket costs, and enrolling during the Open Enrollment Period is the single most important decision you will make about it.

| Point | Details |

|---|---|

| Medigap fills Medicare gaps | It covers deductibles, coinsurance, and copays that Original Medicare leaves unpaid. |

| Plans are federally standardized | Every insurer’s Plan G offers identical benefits; only the premium differs. |

| Enroll during Open Enrollment | The six-month window after Part B enrollment guarantees acceptance without medical underwriting. |

| Medigap excludes key benefits | Prescription drugs, dental, vision, and long-term care require separate coverage. |

| Shop multiple carriers | Comparing premiums for the same plan letter is the fastest way to reduce your monthly cost. |

What I’ve learned advising seniors on Medigap

The most common mistake I see is waiting. Seniors tell me they feel healthy and want to hold off on the monthly premium. I understand that instinct completely. But the Open Enrollment Period does not wait for a convenient moment. It opens and closes on a fixed schedule, and once it closes, your health history becomes fair game for insurers.

The second thing I’ve noticed is that people often confuse Medigap with Medicare Advantage. Many beneficiaries mix up these two products because both involve private insurers and both relate to Medicare. The difference is fundamental. Medigap supplements Original Medicare. Medicare Advantage replaces it. Choosing the wrong product means rebuilding your coverage from scratch.

On the plan selection side, I lean toward Plan G for most seniors who see doctors regularly. The predictability it provides is worth the higher premium for many people. Plan N makes sense if you are generally healthy, rarely see specialists, and want to keep monthly costs lower while still having solid protection. Neither plan is universally right. The correct answer depends on your health, your budget, and how much financial uncertainty you can absorb.

One thing I tell every client: shopping multiple carriers for the same plan letter is not optional, it is the job. The benefits are identical by law. The premiums are not. I have seen the same Plan G cost $80 more per month from one carrier than another in the same zip code. That is nearly $1,000 per year for the same coverage. Xactinsure works with multiple carriers precisely to surface those differences for you.

— Alston

Xactinsure helps you find the right Medigap plan

Choosing between Plan G, Plan N, and other Medigap options is easier with guidance from someone who knows the local market and works with multiple carriers. Xactinsure serves seniors across Fort Myers, Cape Coral, Naples, and neighboring Southwest Florida counties, offering free, no-obligation consultations to help you compare plans and premiums side by side.

Whether you are approaching 65 or already enrolled in Medicare, Xactinsure can walk you through your Medicare supplement options and match you with the plan that fits your health needs and budget. You can also review detailed guides for Plan G coverage or Plan N coverage before your consultation. Schedule a free appointment and get clear answers without pressure.

FAQ

What does Medigap coverage pay for?

Medigap pays for cost-sharing gaps left by Original Medicare, including the $1,736 Part A inpatient deductible and the 20% Part B outpatient coinsurance in 2026. The specific costs covered depend on which lettered plan you hold.

Is Medigap the same as Medicare Advantage?

No. Medigap supplements Original Medicare Parts A and B, while Medicare Advantage replaces Original Medicare with a private plan. You cannot hold both a Medigap policy and a Medicare Advantage plan at the same time.

When is the best time to buy a Medigap policy?

The best time is during your six-month Open Enrollment Period, which begins when you turn 65 and enroll in Medicare Part B. During this window, insurers must accept you regardless of your health history, with no medical underwriting.

Does Medigap cover prescription drugs?

No. Medigap policies do not cover prescription drugs. You need a separate Medicare Part D plan to cover medication costs.

What is the difference between Plan G and Plan N?

Plan G covers nearly all Medicare cost-sharing except the Part B deductible, making it the most comprehensive option for new enrollees. Plan N has lower premiums but includes copays for office and emergency room visits and does not cover Part B excess charges.

Recommended

- Top Reasons to Choose Medigap at Enrollment | XactInsure Blog

- Medicare Supplement Plan G - Guide & Information

- Medicare Preventive Care Coverage Explained for Seniors | XactInsure Blog

- Medicare Insurance Plans Southwest Florida

Get a Free Professional Insurance Review

Our licensed Southwest Florida specialists serve Lee, Collier, and Charlotte counties with local, family-first protection advice.

Request Free Consultation →