Medicare preventive care coverage is defined as a set of health services, screenings, vaccines, and counseling visits that Medicare pays for at little or no cost to help beneficiaries stay healthy before illness develops. The Centers for Medicare and Medicaid Services, known as CMS, governs these benefits under 2026 policy guidelines. Both Original Medicare and Medicare Advantage plans cover preventive services, though the details differ. Understanding what is covered, when to schedule it, and how to avoid unexpected bills can save you hundreds of dollars and protect your health for years to come.

What preventive services does Medicare cover?

Medicare Part B covers a broad range of preventive services organized into four main categories: immunizations, tests and screenings, counseling and therapies, and mental health services. Most of these services cost you nothing when your provider accepts Medicare assignment and bills them correctly as preventive care.

Immunizations covered under Medicare include:

- Flu vaccine (annually)

- Pneumococcal vaccine

- Hepatitis B vaccine

- COVID-19 vaccine

Screenings and tests covered include:

- Diabetes screening

- Colorectal cancer screening

- Mammography (breast cancer)

- Cervical and vaginal cancer screening

- Prostate cancer screening

- Cardiovascular disease screening

- Bone mass measurement (osteoporosis)

- Glaucoma screening

- HIV screening

- Lung cancer screening (low-dose CT scan for eligible beneficiaries)

Counseling and behavioral services covered include:

- Diabetes Self-Management Training (DSMT)

- Smoking and tobacco cessation counseling

- Alcohol misuse counseling

- Obesity screening and counseling

- Nutrition therapy for diabetes or kidney disease

Mental health preventive services include depression screening and behavioral counseling such as tobacco cessation and alcohol misuse counseling. These are often overlooked but carry real value for seniors managing chronic stress or mood changes.

One critical detail: many screenings have eligibility rules tied to your age, personal risk factors, and recommended frequency based on U.S. Preventive Services Task Force (USPSTF) guidelines. A diabetes screening, for example, is covered for beneficiaries with certain risk factors, not automatically for everyone. Ask your doctor which screenings apply to you specifically.

How are Medicare preventive visits different from routine physical exams?

This distinction trips up more seniors than almost any other Medicare question. The confusion is understandable, but the financial consequences of getting it wrong can be significant.

The Initial Preventive Physical Exam (IPPE), sometimes called the “Welcome to Medicare” visit, is a one-time benefit available within the first 12 months of enrolling in Medicare Part B. CMS covers the IPPE with no cost-sharing when your provider accepts assignment. This visit focuses on reviewing your medical and family history, checking your height, weight, blood pressure, and vision, and creating a personalized prevention plan.

The Annual Wellness Visit (AWV) is available once every 12 months after your first year of Part B coverage. Like the IPPE, the AWV costs nothing when billed correctly as a preventive service. It is not a head-to-toe physical. It is a structured conversation with your provider to update your health risk assessment and review your prevention schedule.

Routine physical exams are a different matter entirely. Medicare does not cover routine physicals unrelated to a specific illness or symptom. If you ask your doctor to do a full physical during your AWV, that portion of the visit may be billed separately, and you will pay 100% of that cost out of pocket.

The billing problem arises when a visit starts as preventive but drifts into problem-focused care. CMS explicitly warns that adding diagnostic services to a preventive visit can trigger cost-sharing you did not expect. If your doctor addresses a new complaint during your AWV, that service may be billed as a separate office visit with its own copay.

Pro Tip: Before your visit, tell your provider clearly that you want to keep the appointment coded as a preventive wellness visit. If you have a new concern, ask whether it should be addressed at a separate appointment to protect your zero-cost preventive benefit.

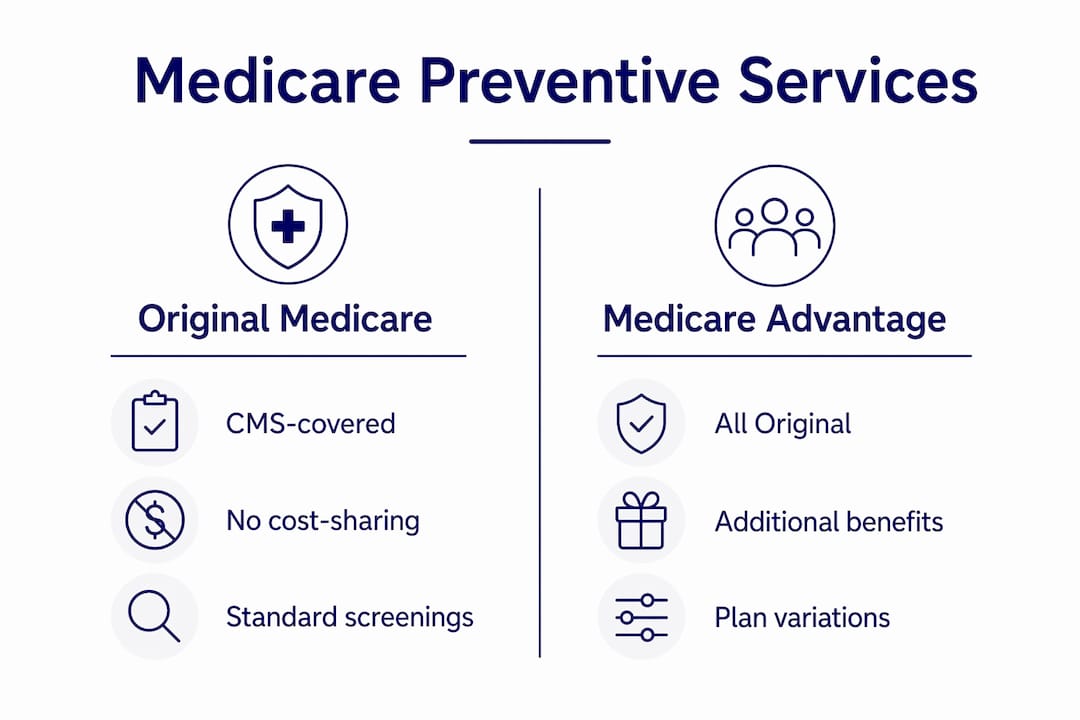

How does preventive coverage differ between Original Medicare and Medicare Advantage?

Choosing between Original Medicare and Medicare Advantage affects more than just your premiums. It shapes how you access preventive care and what you pay for it.

| Feature | Original Medicare | Medicare Advantage |

|---|---|---|

| Preventive services covered | All CMS-approved Part B services | Must cover all Part B services, plus may add more |

| Cost-sharing for preventive care | $0 when billed correctly | $0 for required services; varies for extras |

| Dental, vision, hearing | Not covered | Often included, but with limits |

| Network restrictions | See any Medicare-accepting provider | Usually restricted to plan network |

| Prior authorization | Rarely required | May apply to some services |

| Out-of-pocket cap | No cap | Defined annual limit required by law |

Original Medicare covers the standard CMS preventive services list with no cost-sharing when your provider bills them properly. You can see any doctor who accepts Medicare, which matters greatly for seniors in rural areas or those who travel between states.

Medicare Advantage plans in 2026 must cover at least everything Original Medicare covers, including all preventive services. Many plans go further by adding dental cleanings, eye exams, and hearing aids. That sounds appealing, but those extras often come with network restrictions and coverage limits that vary widely from plan to plan.

Prior authorization in Medicare Advantage is rarely required for standard preventive services, but it can apply to supplemental benefits and some specialist referrals. Caregivers comparing plans for a family member should read the Evidence of Coverage document carefully to understand which services require approval before scheduling. The Medicare Advantage supplemental benefits like dental and vision are commonly offered but often carry limits or network restrictions that reduce their real-world value.

For seniors in Southwest Florida, local Medicare plan options vary by county, and the right choice depends heavily on your doctors, your health needs, and how often you use specialist care.

What steps help you maximize your Medicare preventive benefits?

Getting the most from your preventive coverage requires planning, not luck. These steps give you a clear path forward.

-

Schedule your Welcome to Medicare visit immediately. Missing the IPPE window within the first 12 months of Part B enrollment forfeits that benefit permanently. It cannot be rescheduled or recovered. Call your primary care provider within your first month of coverage.

-

Book your Annual Wellness Visit every year. Set a calendar reminder for the same month each year. The AWV resets annually, and skipping it means losing a free, structured health review that keeps your prevention plan current.

-

Prepare a written list of questions before each visit. Bringing a prepared list tied to CMS preventive service categories helps your provider code the visit accurately. Focus your questions on screenings, vaccines, and risk factors rather than new symptoms or complaints.

-

Confirm preventive billing before you leave. Ask the front desk or your provider to confirm that the visit will be billed as preventive. This one step prevents most surprise bills.

-

Track your screenings and vaccines. Keep a personal health record that lists each screening you have received, the date, and when it is next due. Diabetes screenings, colorectal cancer screenings, and mammograms each have specific frequency rules. Knowing your schedule prevents gaps and duplicate tests.

-

Ask about supplemental coverage for services Medicare does not cover. Routine dental, vision, and hearing care fall outside Original Medicare. A Medicare Supplement plan or a Medicare Advantage plan with strong supplemental benefits can fill those gaps.

Pro Tip: If your doctor addresses a new health concern during your AWV, ask them to document it as a separate encounter. That simple step keeps your wellness visit coded as preventive and protects your zero-cost benefit.

Key takeaways

Medicare preventive care coverage delivers the most value when beneficiaries schedule visits on time, communicate clearly with providers about billing, and understand the difference between preventive and routine care.

| Point | Details |

|---|---|

| IPPE is a one-time benefit | Schedule your Welcome to Medicare visit within 12 months of Part B enrollment or lose it permanently. |

| AWV is free and annual | The Annual Wellness Visit costs nothing when billed correctly and resets every 12 months. |

| Routine physicals are not covered | Medicare pays nothing for routine physical exams; you pay 100% out of pocket for those. |

| Billing determines your cost | A visit coded as diagnostic instead of preventive can trigger unexpected copays. |

| Medicare Advantage adds benefits with trade-offs | Advantage plans may offer dental and vision but often include network limits and prior authorization rules. |

What I’ve learned from years of helping seniors navigate preventive care

Working with Medicare beneficiaries in Southwest Florida, I have seen the same costly mistake repeat itself year after year. A senior schedules what they believe is a free wellness visit, mentions a new knee pain to their doctor, and walks out with a bill they never expected. The visit was no longer coded as purely preventive. That surprise charge was entirely avoidable.

The IPPE is the most underused benefit in all of Medicare. Newly eligible beneficiaries often do not know it exists, or they assume it is the same as a routine physical and skip it. It is not the same. It is a structured, covered benefit with a hard deadline. Missing it is like leaving money on the table and locking the drawer behind you.

I also see caregivers who manage appointments for aging parents underestimate how much the billing conversation matters. Correct documentation by the provider directly determines whether a visit stays covered. You have every right to ask how a visit will be billed before it happens. That is not being difficult. That is being an informed patient.

CMS updates its preventive services list periodically, and 2026 brought continued refinements to coverage categories. Staying current with those changes is part of protecting your benefits. Read the annual Medicare and You handbook when it arrives, or ask a licensed agent to walk you through what changed.

— Alston

How Xactinsure helps you get the most from your Medicare coverage

Knowing your preventive benefits is one thing. Choosing the right plan to support them is another.

Xactinsure specializes in Medicare coverage for seniors across Fort Myers, Cape Coral, Naples, and surrounding Southwest Florida communities. The team works with multiple carriers to compare Original Medicare, Medicare Advantage, and Medicare Supplement plans side by side, so you see exactly what each option covers and what it costs. Whether you are newly eligible or reconsidering your current plan, a free consultation with Xactinsure gives you a clear picture of your preventive care benefits, your out-of-pocket exposure, and the plan that fits your health and budget. Schedule a consultation and get answers tailored to your situation.

FAQ

What is the Welcome to Medicare visit?

The Welcome to Medicare visit, formally called the Initial Preventive Physical Exam (IPPE), is a one-time covered visit available within the first 12 months of Medicare Part B enrollment. It costs nothing when your provider accepts Medicare assignment and focuses on building a personalized prevention plan.

Does Medicare cover routine physical exams?

No. Medicare does not cover routine physical exams unrelated to illness or symptoms. Beneficiaries pay 100% of the cost for those exams out of pocket.

How often can I get an Annual Wellness Visit?

Medicare covers one Annual Wellness Visit every 12 months after your first year of Part B coverage. The visit is free when billed as a preventive service by a provider who accepts Medicare assignment.

Does Medicare Advantage cover the same preventive services as Original Medicare?

Yes. Medicare Advantage plans must cover all preventive services included in Original Medicare. Many plans also add dental, vision, and hearing benefits, though those extras vary by plan and may include network restrictions.

What happens if my preventive visit includes a diagnostic service?

Adding a diagnostic service to a preventive visit can result in a separate bill with its own cost-sharing. Ask your provider to schedule any new health concerns as a separate appointment to keep your preventive visit fully covered.

Recommended

- Insurance Articles & Guides - XactInsure Blog

- Medicare Insurance Plans in Cape Coral, Florida

- Medicare Insurance Plans & Guidance - XactInsure

- Medicare Insurance Plans Southwest Florida

Get a Free Professional Insurance Review

Our licensed Southwest Florida specialists serve Lee, Collier, and Charlotte counties with local, family-first protection advice.

Request Free Consultation →