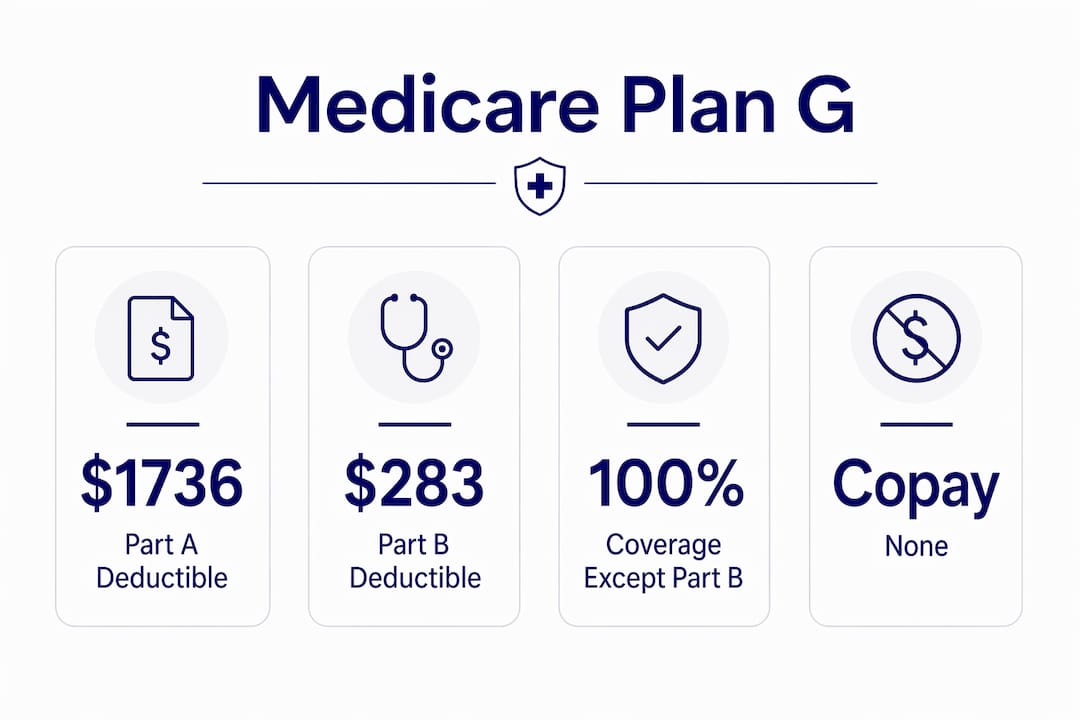

Medicare Plan G is defined as a Medicare Supplement (Medigap) insurance policy that covers nearly all out-of-pocket costs left by Original Medicare, with one exception: the annual Part B deductible. For 2026, that deductible is $283. Once you pay that single annual amount, Plan G covers the rest. No copays. No coinsurance. No surprise hospital bills. For seniors who want predictable healthcare costs, Plan G’s comprehensive coverage makes it the most complete Medigap option available to anyone who became Medicare-eligible on or after january 1, 2020.

What does Medicare Plan G cover in 2026?

Medicare Plan G is the most comprehensive plan for beneficiaries eligible on or after january 1, 2020. It covers all Medicare cost-sharing except the $283 Part B deductible. That single annual payment is the only out-of-pocket expense you face for covered services.

Plan G covers the following costs that Original Medicare leaves unpaid:

- Part A hospital deductible: $1,736 per benefit period in 2026

- Part A coinsurance and hospital costs: Up to 365 additional days after Medicare benefits end

- Skilled nursing facility coinsurance: Days 21 through 100 of a covered stay

- Part B coinsurance or copayment: 20% of Medicare-approved costs for doctor visits, outpatient services, and procedures

- Part B excess charges: Up to 15% above Medicare-approved amounts when a provider does not accept Medicare assignment

- Foreign travel emergency coverage: 80% of billed charges after a small deductible, up to plan limits

The Part A deductible alone is $1,736 per benefit period. A single hospitalization without Plan G could cost you that amount before Medicare pays a cent. Plan G eliminates that exposure entirely.

Pro Tip: Plan G does not include prescription drug coverage. You will need a separate Part D plan for medications. Factor that premium into your total monthly budget when comparing costs.

What are the benefits of choosing Medicare Plan G?

The primary benefit of Plan G is cost predictability. After you pay the $283 Part B deductible once per year, you owe nothing more for Medicare-covered services. That structure protects you from the kind of unexpected bills that can follow a hospitalization, surgery, or extended specialist care.

Part B excess charges deserve special attention. When a doctor does not accept Medicare assignment, they can legally bill up to 15% above Medicare-approved amounts. Plan G covers those charges in full. That protection matters most in areas with a high concentration of non-participating providers, which includes parts of Southwest Florida.

Plan G also shines for seniors with active healthcare needs. If you see specialists regularly, manage a chronic condition, or anticipate surgery, the math favors Plan G quickly. A few specialist visits per month at 20% coinsurance can add up to hundreds of dollars without supplemental coverage. Plan G eliminates that math entirely after your deductible.

Plan F, the previous gold-standard Medigap plan, is closed to new enrollees who became eligible after december 31, 2019. That closure has pushed Plan F premiums higher as its pool of insured members ages. Plan G now fills that role for new beneficiaries, often at a lower premium than Plan F charges its existing members.

Pro Tip: Keep a simple annual tally of your Medicare-covered medical expenses. If your total out-of-pocket costs under a lower-premium plan would exceed what you pay for Plan G, Plan G is the better financial choice.

How does Plan G compare to Plan N?

Plan G and Plan N are the two most popular Medigap options for new Medicare beneficiaries. They share the same foundation but differ in two key areas: copays and excess charge coverage.

| Coverage Feature | Plan G | Plan N |

|---|---|---|

| Part B deductible | Not covered ($283 you pay) | Not covered ($283 you pay) |

| Part B coinsurance | Covered in full | Covered, with copays |

| Office visit copay | None | Up to $20 per visit |

| Emergency room copay | None | Up to $50 per visit |

| Part B excess charges | Covered in full | Not covered |

| Part A deductible | Covered in full | Covered in full |

| Skilled nursing coinsurance | Covered in full | Covered in full |

| Average monthly premium (age 65) | ~$220/month | ~$171/month |

Plan G averages $220 per month versus $171 for Plan N at age 65. That $49 monthly difference totals $588 per year. Whether Plan N’s lower premium saves you money depends entirely on how often you use medical services and whether your providers bill excess charges.

Frequent medical visits with Plan N’s copays can erode those premium savings faster than most people expect. Copays and excess charges with Plan N could add up to $36,000 more over a 20-year retirement compared to Plan G. That figure assumes regular medical use and exposure to excess charges. For a senior with minimal healthcare needs, Plan N may still come out ahead. For anyone managing ongoing conditions, Plan G typically wins.

Pro Tip: Review your current doctor list before choosing Plan N. If any of your providers do not accept Medicare assignment, you face excess charges that Plan N will not cover. Check Medicare’s physician compare tool or call each office directly.

When and how should you enroll in Medicare Plan G?

Enrollment timing is the single most important factor in getting Plan G without complications. The rules are clear and the window is finite.

-

Identify your Medigap Open Enrollment Period. This six-month window begins the first month you are both 65 and enrolled in Medicare Part B. It does not repeat. It does not extend.

-

Apply during the open enrollment window. During this period, insurers must sell you any Medigap policy at standard rates. They cannot ask about your health history, charge you more for pre-existing conditions, or deny your application.

-

Compare premiums across carriers. Medigap benefits are federally standardized, meaning every Plan G policy covers the same services regardless of which insurer sells it. The only differences are the monthly premium and the insurer’s reputation for rate stability.

-

Submit your application before the window closes. Most insurers process applications within a few weeks. Time your application so coverage begins the month your Part B starts.

-

Understand what happens if you miss the window. Missing the open enrollment period means insurers can require full medical underwriting. They can deny your application, exclude pre-existing conditions, or charge significantly higher premiums based on your health status.

The guaranteed issue right during open enrollment is one of the most valuable protections in Medicare. Missing it can mean paying more for less coverage, or being turned down entirely. Enrolling on time at Medigap open enrollment is the single most protective financial step a new Medicare beneficiary can take.

What practical factors should seniors consider when selecting Plan G?

Choosing Plan G wisely requires looking beyond the monthly premium. Several factors shape whether Plan G delivers its full value for your specific situation.

Your healthcare utilization pattern matters most. A senior who sees multiple specialists, manages a chronic illness, or anticipates a procedure will reach Plan G’s break-even point quickly. A senior in excellent health with minimal doctor visits may find a lower-premium option more cost-effective in the short term.

Your location affects excess charge exposure. Some states ban or limit Medicare Part B excess charges by law. In those states, Plan G’s excess charge protection adds less practical value. Florida does not ban excess charges, which means Southwest Florida seniors face real exposure without Plan G’s protection.

Consider these additional factors before finalizing your choice:

- High-Deductible Plan G: This option carries the same coverage as standard Plan G but requires you to pay a $2,950 deductible before benefits apply. Premiums are significantly lower. It suits seniors who want catastrophic protection but are comfortable covering routine costs out of pocket.

- Insurer premium stability: All Plan G policies cover the same benefits, but insurers raise premiums at different rates over time. Ask about historical rate increases before choosing a carrier.

- Prescription drug coverage: Plan G does not cover medications. You need a standalone Part D plan. Review 2026 Medicare costs to budget accurately for both premiums together.

- No network restrictions: Plan G works with any provider who accepts Medicare, nationwide. That matters for snowbirds and anyone who travels or splits time between states.

Pro Tip: Ask any insurer you consider for their rate increase history over the past five years. A lower premium today means little if the carrier raises rates aggressively each year.

Key takeaways

Medicare Plan G is the most comprehensive Medigap plan for new beneficiaries, covering all Medicare cost-sharing except the $283 annual Part B deductible, making it the clearest path to predictable healthcare costs in retirement.

| Point | Details |

|---|---|

| Plan G coverage scope | Covers all Medicare gaps except the $283 Part B deductible, including Part A costs and excess charges. |

| Enrollment timing | The six-month Medigap Open Enrollment Period at age 65 guarantees coverage with no medical underwriting. |

| Plan G vs. Plan N | Plan G costs ~$49 more per month but eliminates copays and covers excess charges Plan N does not. |

| High-Deductible option | High-Deductible Plan G lowers premiums but requires a $2,950 deductible before benefits apply. |

| Insurer comparison | All Plan G policies cover identical benefits; compare carriers on premium stability, not coverage. |

Why Plan G is the plan I recommend most often

After working with hundreds of seniors in Southwest Florida, I keep coming back to the same observation: most people underestimate their exposure to Part B excess charges. They assume their doctors all accept Medicare assignment. Many do not, especially specialists in Fort Myers, Naples, and Cape Coral. One unexpected excess charge from a cardiologist or orthopedic surgeon can wipe out months of premium savings from a lower-cost plan.

The other mistake I see regularly is focusing only on the monthly premium. A $49 monthly difference between Plan G and Plan N sounds meaningful. But if you visit a specialist four times a year and face two excess charge situations, that gap closes fast. Financial planners advise evaluating total healthcare utilization, not just monthly premiums, when selecting between Medigap plans. That advice is right.

Plan G is not perfect for everyone. A healthy 65-year-old with minimal medical needs and a tight budget may do well with High-Deductible Plan G or Plan N for a few years. But for most new Medicare beneficiaries, Plan G’s combination of broad coverage and cost certainty is hard to beat. The $283 annual deductible is a small, known cost. Everything else is covered. That simplicity has real value when you are managing your health in retirement.

My strongest advice: do not wait. The Medigap Open Enrollment Period is the only time you are guaranteed the right to buy Plan G at standard rates. Miss it, and your health history becomes a factor. Enroll on time, compare carriers on premium stability, and you will have coverage you can count on for years.

— Alston

Xactinsure can help you find the right Plan G coverage

Choosing between Plan G, Plan N, and other Medigap options is straightforward when you have the right guidance. Xactinsure works with multiple carriers across Southwest Florida, including Fort Myers, Cape Coral, and Naples, to find you the best premium for the same standardized Plan G benefits.

Xactinsure offers free, no-obligation consultations to walk you through your options, compare carrier premiums side by side, and answer every question before you enroll. There is no pressure and no guesswork. Whether you are turning 65 next month or helping a parent sort through their choices, the team at Xactinsure is ready to help. Schedule a consultation or visit the Medicare Plan G guide to get started with personalized support today.

FAQ

What does Medicare Plan G cover in 2026?

Medicare Plan G covers all Medicare cost-sharing except the $283 annual Part B deductible, including the Part A hospital deductible, Part B coinsurance, skilled nursing facility coinsurance, and Part B excess charges.

Is Medicare Plan G worth the higher premium over Plan N?

Plan G costs approximately $49 more per month than Plan N at age 65, but it eliminates all copays and covers excess charges that Plan N does not. Seniors with regular medical needs typically find Plan G the better value over time.

What happens if I miss the Medigap Open Enrollment Period?

Missing the six-month open enrollment window means insurers can apply medical underwriting, potentially denying coverage or charging higher premiums based on your health history. Enrolling on time guarantees standard rates regardless of health status.

What is High-Deductible Plan G?

High-Deductible Plan G provides the same coverage as standard Plan G but requires you to pay a $2,950 deductible before benefits apply, in exchange for significantly lower monthly premiums.

Does Plan G cover prescription drugs?

Plan G does not include prescription drug coverage. Beneficiaries need a separate Medicare Part D plan to cover medications, which should be factored into the total monthly insurance budget.

Recommended

- Medicare Supplement Plan G - Guide & Information

- Medicare Options for Aging Parents: 2026 Family Guide | XactInsure Blog

- Medicare Insurance Plans & Guidance - XactInsure

- Medicare Insurance Plans in Golden Gate

Get a Free Professional Insurance Review

Our licensed Southwest Florida specialists serve Lee, Collier, and Charlotte counties with local, family-first protection advice.

Request Free Consultation →