Medicare and assisted living coverage is one of the most misunderstood topics in senior healthcare planning. Medicare pays $0 toward assisted living room and board costs, a fact that catches many families off guard when the bills arrive. Knowing exactly what Medicare does and does not cover, and how programs like Medicaid and long-term care insurance fill the gaps, is the foundation of sound financial planning for any senior considering assisted living. This guide breaks down the rules clearly so you can make confident decisions for yourself or a loved one.

What does Medicare cover in assisted living settings?

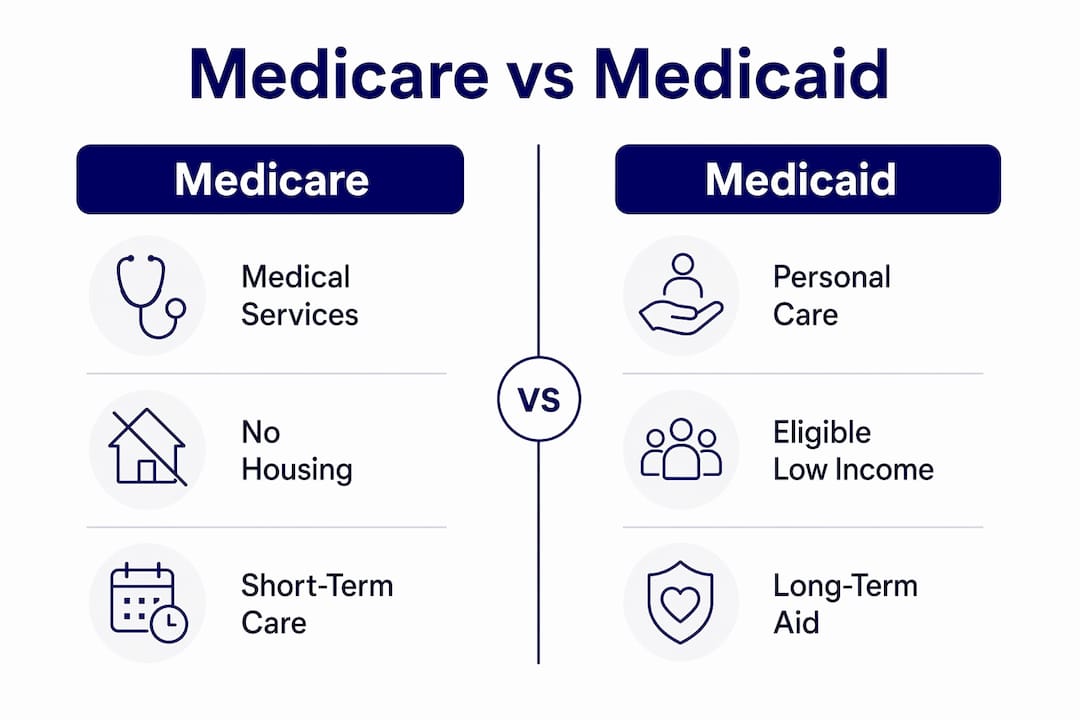

Medicare covers medical services, not housing or personal care. Original Medicare Parts A and B cover hospital stays, doctor visits, skilled nursing care after a qualifying hospital stay, and limited home health services. Those benefits follow the person, meaning a resident in an assisted living facility can still use them for covered medical needs. What Medicare will never pay for is the room, the meals, or the help with bathing and dressing.

The distinction that matters most is medical care versus custodial care. Medicare covers medically necessary services ordered by a physician. Custodial care, which includes help with daily activities like dressing, grooming, and medication reminders, falls entirely outside Medicare’s scope. Most of what assisted living facilities provide is custodial care.

Here is what Medicare does and does not cover for assisted living residents:

Medicare covers:

- Inpatient hospital stays under Part A

- Doctor visits and outpatient services under Part B

- Skilled nursing facility care for up to 100 days after a 3-day hospital stay

- Home health services (physical therapy, skilled nursing visits) when medically necessary

- Durable medical equipment like wheelchairs or walkers

Medicare does not cover:

- Monthly room and board fees

- Assistance with activities of daily living (bathing, dressing, eating)

- Long-term custodial care of any kind

- Memory care unit fees

- Most personal care services

Medicare Advantage plans include all Original Medicare benefits plus some supplemental services, but they do not cover assisted living costs directly. Some plans offer extras like meal delivery or transportation, but coverage varies significantly by plan and carrier. Families should review the Summary of Benefits for any Medicare Advantage plan carefully before assuming it covers assisted living needs.

Pro Tip: If a loved one moves into assisted living after a hospital stay of three or more days, Medicare Part A may cover skilled nursing facility care for a limited time. That window is short, so act quickly to verify eligibility with the facility’s billing team.

Why doesn’t Medicare pay for assisted living, and how does Medicaid compare?

Medicare is federal health insurance designed to cover acute medical care. It was never built to fund long-term housing or personal assistance. Understanding that distinction removes a lot of confusion and helps families plan realistically.

Medicaid operates differently. It is a joint federal and state program for people with limited income and assets. Medicaid waivers may cover some personal care or therapy services inside assisted living facilities, but federal law prohibits Medicaid from paying room and board directly. Even when Medicaid covers care services, residents typically pay their own income toward housing costs. Medicaid covers care services for roughly 15–17% of assisted living residents, and eligibility requires meeting strict financial and medical criteria.

Long-term care insurance is a private product purchased before care is needed. It can pay for assisted living room and board, personal care, and other custodial services that Medicare excludes. Premiums rise sharply with age, so purchasing a policy in your 50s or early 60s produces the best value.

| Coverage type | What it pays for | Key limitation |

|---|---|---|

| Medicare (Parts A and B) | Medical services, skilled nursing, hospital stays | Does not cover custodial care or room and board |

| Medicare Advantage | Original Medicare benefits plus limited extras | Does not cover assisted living costs directly |

| Medicaid | Some care services via state waivers | Cannot pay room and board; strict income and asset limits |

| Long-term care insurance | Room, board, and personal care | Must be purchased before care is needed; premiums increase with age |

Pro Tip: Consulting an elder law attorney before spending down assets for Medicaid eligibility can protect more of a family’s wealth. Medicaid spend-down rules are complex, and legal guidance can make a significant financial difference.

What do assisted living facilities actually cost in 2026?

Assisted living costs have risen steadily, and the numbers are significant. The national median cost of assisted living in 2026 is $5,419 per month, up 4.4% from the prior year. That translates to roughly $65,000 annually before accounting for additional care charges. Monthly costs range from approximately $4,000 in lower-cost states to over $9,000 in high-cost markets like California or New York.

Pricing models vary between facilities, and the model a facility uses affects your long-term budget significantly.

- All-inclusive pricing bundles housing, meals, and a set level of care into one flat monthly rate. It offers predictability but may include services a resident does not need.

- Tiered pricing starts with a base rate and adds charges as care needs increase. As a resident requires more assistance, monthly fees can rise by $500 to $2,500 above the base rate.

Beyond the monthly fee, most facilities charge a one-time community fee at move-in. That upfront fee typically ranges from $2,000 to $10,000 and is not covered by any insurance. It is one of the most commonly overlooked costs in assisted living budgeting.

Additional variable charges often include:

- Medication management fees

- Incontinence supply charges

- Transportation to medical appointments

- Extra housekeeping or laundry services

- Memory care unit premiums

Requesting a complete, itemized fee schedule before signing any contract is the single most effective way to avoid billing surprises. Ask specifically what triggers a care level increase and how much each level costs.

How can seniors and families finance assisted living?

Out-of-pocket payment is the most common method families use to cover assisted living costs. Retirement savings, Social Security income, pension payments, and proceeds from selling a home all contribute. For many families, a combination of sources is necessary from the start.

Several programs and products can reduce the financial burden:

- Medicaid Home and Community-Based Services (HCBS) waivers allow states to fund personal care services inside assisted living for eligible low-income seniors. Availability varies by state, and waitlists are common.

- Veterans benefits, specifically the VA Aid and Attendance benefit, provide monthly payments to qualifying veterans and surviving spouses to help cover assisted living costs. The benefit is underused and worth investigating early.

- Medicare Advantage supplemental benefits may cover limited services like transportation or meal delivery, reducing some out-of-pocket expenses. Review Medicare coverage options carefully to understand what a specific plan actually includes.

- Long-term care insurance pays directly to the facility for covered services, reducing the draw on personal savings.

- Life insurance policy conversions allow some seniors to convert existing life insurance into funds for long-term care, either through a life settlement or a policy rider.

Early planning is the most powerful financial tool available. Families who begin researching costs and coverage options five or more years before care is needed have far more choices than those who plan reactively. An elder law attorney can help structure assets to preserve Medicaid eligibility without violating look-back rules.

Pro Tip: The VA Aid and Attendance benefit does not require a service-related disability. Any veteran who served during a wartime period and needs help with daily activities may qualify. Many eligible seniors never apply because they do not know the benefit exists.

Key takeaways

Medicare does not cover assisted living room and board costs, making early financial planning with Medicaid waivers, long-term care insurance, and veterans benefits the only reliable path to managing these expenses.

| Point | Details |

|---|---|

| Medicare covers medical care only | Room, board, and custodial care are excluded from all Medicare plans. |

| Medicaid covers services, not housing | State waivers may fund personal care, but residents pay their own housing costs. |

| 2026 median cost is $5,419/month | Costs range from $4,000 to over $9,000 depending on location and care level. |

| Community fees are often overlooked | Move-in fees of $2,000 to $10,000 are not covered by any insurance product. |

| Early planning expands your options | Long-term care insurance and Medicaid planning work best when started years in advance. |

The misconception that costs families the most

Families come to me with the same assumption almost every week: Medicare will cover assisted living when the time comes. That belief is understandable. Medicare covers so much of senior medical care that it feels like it should extend to housing and daily assistance too. It does not, and the gap between expectation and reality can be financially devastating.

The families who handle this best are the ones who stop thinking about assisted living as a medical expense and start treating it as a housing and lifestyle expense with a medical component. Medicare handles the medical component well. The housing piece requires a completely separate plan.

What I have seen work consistently is a layered approach. Long-term care insurance covers the custodial portion. A Medicare Supplement plan like Plan G handles the medical gaps. Veterans benefits or Medicaid waivers fill in where other coverage falls short. No single product solves the whole problem, and anyone who tells you otherwise is oversimplifying.

The other mistake I see is waiting too long to consult a professional. Medicaid planning has a five-year look-back period. Long-term care insurance premiums double or triple between age 55 and 70. The cost of waiting is real and measurable. The families who act early, even if care is still a decade away, consistently end up with better options and lower total costs.

— Alston

Xactinsure can help you find the right Medicare plan

Choosing the right Medicare plan is one of the most consequential financial decisions a senior makes. The wrong plan leaves gaps that cost thousands of dollars when care is needed most.

Xactinsure works with seniors and families across Southwest Florida, including Fort Myers, Cape Coral, and Naples, to find Medicare coverage that fits real needs and real budgets. The team compares plans across multiple carriers to give you an honest picture, not a sales pitch. Whether you need help understanding Medicare Supplement options, want to review what a Medicare Advantage plan actually covers, or are ready to sit down with an expert, Xactinsure offers free, no-obligation consultations. You can also attend one of the free educational seminars designed specifically for seniors and their families. Getting the right coverage starts with a single conversation.

Schedule your free consultation today and get clear answers about your options.

FAQ

Does Medicare pay for assisted living room and board?

No. Medicare pays $0 toward assisted living room and board costs. Medicare covers only medical services, not housing or custodial care.

What is the difference between Medicare and Medicaid for assisted living?

Medicare covers medical care for seniors regardless of income. Medicaid covers some personal care services for low-income seniors through state waivers, but federal law prohibits it from paying room and board directly.

How much does assisted living cost per month in 2026?

The national median cost is $5,419 per month in 2026. Costs range from roughly $4,000 to over $9,000 depending on location and the level of care required.

Does Medicare Advantage cover assisted living?

Medicare Advantage plans do not cover assisted living costs directly. Some plans offer limited supplemental benefits like transportation or meal delivery, but full assisted living coverage is not included in any Medicare Advantage plan.

What is the best way to pay for assisted living?

Most families use a combination of personal savings, long-term care insurance, and Medicaid waivers. Veterans may also qualify for the VA Aid and Attendance benefit. Early planning and professional guidance from an elder law attorney produce the best financial outcomes.

Recommended

- Medicare Options for Aging Parents: 2026 Family Guide | XactInsure Blog

- Medicare and Respiratory Care Coverage: 2026 Guide | XactInsure Blog

- Medicare Costs Every Family Should Understand in 2026 | XactInsure Blog

- What Is Medicare Managed Care? A Clear Guide for Seniors | XactInsure Blog

Get a Free Professional Insurance Review

Our licensed Southwest Florida specialists serve Lee, Collier, and Charlotte counties with local, family-first protection advice.

Request Free Consultation →